Ocean Carrier Consolidation Is Changing Freight Costs in 2026

If your ocean freight costs have been climbing, you are not imagining it. Rates on several major trade lanes have moved sharply higher heading into June 2026, and space is getting tighter on key routes.

Part of the pressure comes from stronger demand, blank sailings, and new rate increases. But there is a bigger issue behind the scenes. Fewer carriers now control most of the world’s container shipping capacity. That gives the largest carriers more influence over space, service options, and pricing than they had years ago.

For importers and exporters, this does not mean you are out of options. It means your freight strategy needs to be more informed, more flexible, and more closely managed. At Southern Star Navigation, we track these changes every day, so our clients are never caught off guard.

Who Controls the Seas Right Now?

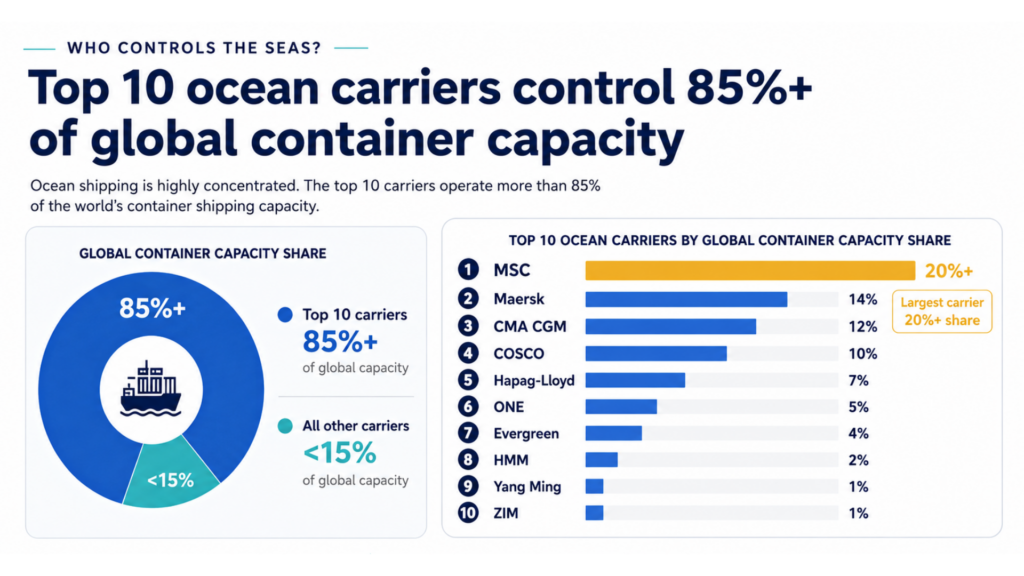

The container shipping industry is highly concentrated. The top 10 ocean carriers now control more than 85% of all global container capacity. One company alone, MSC (the Mediterranean Shipping Company), holds more than a 20% share of the worldwide market. The next largest are Maersk, CMA CGM, COSCO, and Hapag-Lloyd.

MSC operates roughly 887 ships with a total capacity of approximately 6.4 million TEUs. A TEU is a standard 20-foot container unit, the basic measurement of shipping capacity. Maersk holds the number two spot, with CMA CGM expected to move into second place as new vessels in its orderbook are delivered.

When a handful of companies control most of the ships, containers, and routes, they have significant leverage over pricing. That concentration is increasing, and the deals being signed right now are making it more pronounced.

The Hapag-Lloyd and ZIM Deal Could Reshape the Market

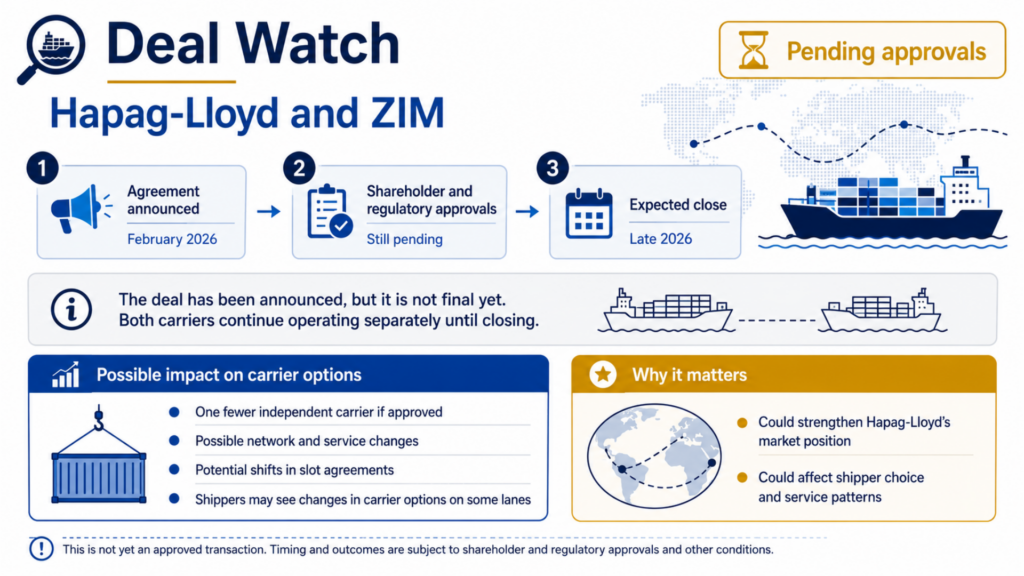

On February 16, 2026, Hapag-Lloyd announced a merger agreement to acquire ZIM Integrated Shipping Services, the world’s 10th largest container line, in an all-cash deal valued at approximately $4.2 billion, or $35 per share. That price represented a 58% premium to ZIM’s stock price the day before the announcement.

ZIM’s board unanimously approved the deal, and ZIM shareholders voted in favor by approximately 97% on April 30, 2026. The transaction still requires regulatory approvals from multiple governments, including Israeli authorities, and is expected to close by late 2026. Until then, both carriers continue to operate independently as competitors.

If approved, the combined carrier would operate a fleet of more than 400 vessels with a total capacity exceeding 3 million TEUs and an estimated annual cargo volume of more than 18 million TEUs. Hapag-Lloyd described ZIM as a strong strategic fit across the Transpacific, Intra-Asia, Latin American, and East Mediterranean trade lanes.

One important detail: ZIM currently has vessel sharing agreements with MSC on six Transpacific services. If the acquisition closes, those ZIM volumes would be expected to shift onto the Gemini network, the alliance between Maersk and Hapag-Lloyd. That is a meaningful shift in capacity alignment on one of the busiest trade lanes in the world.

At Southern Star Navigation, we are monitoring every development in this deal and can advise clients on how it may affect their carrier relationships and bookings.

Other Consolidation Moves to Watch

The Hapag-Lloyd and ZIM deal is the largest headline, but it is not the only significant move happening right now.

On March 10, 2026, Ocean Network Express (ONE) announced it had signed agreements to acquire an additional stake in Poseidon Corp., the parent company of Seaspan Corporation. Seaspan is the world’s largest independent owner of container ships, with a fleet of 227 vessels chartered to virtually every major carrier. The transaction, valued at $1.91 billion, would bring ONE’s total ownership stake in Poseidon to 48.9%. It remains subject to regulatory approval and has not yet been confirmed as closed.

Separately, in February 2026, MSC’s subsidiary SAS Lux signed an investment framework agreement to acquire a 50% stake in Sinokor Merchant Marine, a South Korean shipping group. The deal was notified to competition authorities in Greece and Cyprus. Sinokor operates a large container fleet across Asia, as well as tankers and bulk carriers. Regulatory approvals are still pending, and the transaction has not been confirmed as closed.

The pattern across these moves is consistent. The largest carriers are not just growing their own fleets. They are acquiring ownership stakes in the companies that supply tonnage and operate supporting infrastructure across the entire shipping ecosystem.

How Alliances Affect Your Service Options

Beyond outright ownership, carriers also cooperate through formal alliances. Alliances do not allow carriers to coordinate rates, which would violate antitrust law. What they do allow is sharing space on each other’s vessels, coordinating ship rotations, and running joint services on major trade lanes.

As of June 2026, three main alliances are operating, plus MSC operating on its own.

The Gemini Cooperation is the partnership between Maersk and Hapag-Lloyd, launched in February 2025 with approximately 340 vessels and 3.7 million TEUs of capacity, representing about 21% of the global market. It is built around a hub-and-spoke model and a stated goal of schedule reliability above 90% once fully phased in. If the ZIM acquisition closes, ZIM’s volumes are expected to move into the Gemini network.

The Ocean Alliance includes CMA CGM, COSCO, OOCL, and Evergreen. It is the largest alliance by capacity, deploying nearly 5 million TEUs across 390 vessels with 41 weekly service loops. The agreement runs through 2032.

The Premier Alliance is the partnership of ONE, HMM (Hyundai Merchant Marine), and Yang Ming, which took effect on February 9, 2025 under a five-year agreement. It holds approximately 20% of the global market.

MSC operates independently. Despite being the world’s largest carrier by a wide margin, MSC is not part of any of the three alliances and instead pursues selective arrangements with individual partners.

For shippers, the alliance structure affects which ports are served, how frequently they are called, and how much flexibility exists when problems arise. Southern Star Navigation works across all three alliances, which gives our clients more options when routing decisions need to be made quickly.

What Is a GRI and Why Does It Keep Going Up?

A General Rate Increase, or GRI, is a carrier-announced increase to their base freight rate on a specific trade lane. It applies to the core ocean freight charge before any other add-ons, such as fuel adjustments or terminal handling fees.

GRIs are stated as a fixed dollar amount per TEU or FEU (a 40-foot container). In recent months, announced GRIs have ranged from $500 to $2,000 or more per FEU depending on the lane and the carrier. So if you were paying $3,000 per FEU from Asia to the US West Coast and an $800 GRI goes into effect, your new base rate becomes $3,800 before any additional charges are layered on top.

Under the Shipping Act and FMC regulations, carriers are required to publish tariff changes that result in increased costs to shippers at least 30 days before the effective date (46 CFR 520.8). That rule carried real weight in March 2026, when the Federal Maritime Commission rejected requests from CMA CGM, Hapag-Lloyd, Maersk, and ZIM to shorten that notice period for war-risk surcharges tied to the Strait of Hormuz conflict. The FMC upheld the full 30-day requirement, giving shippers more planning time than carriers would have preferred.

One more distinction worth knowing: a GRI is different from a Peak Season Surcharge (PSS). A GRI is an adjustment to the base rate. A PSS is a temporary add-on tied to a specific high-demand period. Right now in June 2026, many shippers are being charged both at the same time.

What Is Happening With Rates in June 2026?

Rates have climbed sharply heading into June. The Drewry World Container Index, a widely used benchmark for procurement teams, surged 23% to $3,433 per 40-foot container on June 4, 2026, driven by rate increases on the Transpacific and Asia-Europe trade routes. Drewry confirmed that peak season demand started earlier than usual this year.

On specific lanes, Shanghai to Los Angeles rose 31% in a single week to $4,565 per 40-foot container, and Shanghai to New York increased 20% to $5,505. According to Freightos, spot rates across many ex-Asia lanes have been running approximately 20% higher than a year ago.

Several factors are driving this simultaneously. The US-China tariff truce announced in May 2026 triggered a surge in front-loading as importers rushed to move cargo within the 90-day window. That demand surge hit at the same time carriers had already implemented blank sailings of 10 to 15% on Transpacific services to support their mid-May GRI push. Available space tightened quickly.

Adding significant pressure across multiple lanes is the ongoing effective closure of the Strait of Hormuz. As of June 3, 2026, commercial shipping traffic through the strait had collapsed to roughly 10 transits per day against a normal baseline of approximately 95, now more than 95 days into the disruption following the outbreak of the US-Iran conflict in late February. Most major carriers remain unwilling to transit, and the US has indicated mine-clearing operations alone could take six months. Carriers are passing higher operating costs on through war-risk surcharges and emergency fuel adjustments, which stack on top of existing GRIs and peak season charges.

The Southern Star Navigation team is monitoring rates, blank sailings, and space availability across all major lanes on an ongoing basis. If you have shipments planned for the coming weeks, the time to act is now.

What This Means for Importers and Exporters

The effects of consolidation on your shipping program are practical and immediate.

You have fewer carrier choices. On many trade lanes, only two or three realistic service options exist, and they are often operated by the same alliance. When one carrier blanks sailings or adjusts its network, your alternatives are limited.

Route changes are happening. Alliance restructuring can mean discontinued port calls, shifts from direct to transshipment service, and longer transit times. Shippers who relied on a specific routing may find that service has changed or is no longer available.

Negotiating leverage has shifted. When you sit across the table from a top-five carrier to negotiate a contract, you are dealing with a company that controls a significant share of global container capacity. Deep market knowledge and established carrier relationships are your strongest tools in that conversation. That is exactly what Southern Star Navigation brings to every negotiation on behalf of our clients.

Budget planning is harder. A single GRI can add $1,000 or more to the cost of a container, and those announcements can come multiple times per quarter. Businesses budgeting based on contracted rates from 12 months ago are getting expensive surprises in 2026.

How to Protect Your Shipping Program

You cannot change how the shipping industry is structured, but there are practical steps that reduce your exposure.

Book early. Peak season is already arriving ahead of schedule in 2026. If you have shipments planned for June, July, or August, waiting will cost you. Rolled cargo and missed delivery windows can be far more expensive than the freight itself.

Do not rely on a single carrier or alliance. Spreading your cargo across more than one alliance means that when one carrier blanks sailings or changes its network, you have somewhere to go. Southern Star Navigation maintains working relationships across all three alliances and with MSC, which gives our clients real alternatives when the preferred routing falls through.

Review your service contract. Not all contracts are equal. Some include GRI caps or rate stability provisions. Others leave you exposed to every announced increase. If your contract has not been reviewed in the context of today’s market, that is worth doing now.

Look at the full cost, not just the base rate. GRIs, Peak Season Surcharges, war-risk surcharges, and fuel adjustments stack quickly. A rate that looks competitive on the quote can look very different on the invoice. Make sure you are comparing total costs when evaluating options.

Work with a partner who tracks the market daily. Carriers must publish tariff increases at least 30 days in advance under FMC rules. Knowing those windows and timing bookings accordingly can save hundreds to thousands of dollars per container. Southern Star Navigation monitors those filings as a standard part of our work for clients.

The Bottom Line

Ocean shipping in 2026 is more concentrated, more expensive, and harder to navigate independently than it has been in years. A small number of carriers control most of the world’s capacity. Rates are climbing. Alliances have shifted. And the Hapag-Lloyd and ZIM deal, if it clears regulatory approval, could further reshape competitive dynamics on several key trade lanes.

Understanding how all of this connects to your costs, your service options, and your supply chain is the work Southern Star Navigation does every day. Whether you are moving a few containers a month or hundreds, we bring the market knowledge and carrier relationships that help you stay ahead of changes instead of reacting to them.

If your current freight strategy was built for a different market, it may be time for a conversation.

Contact Bethany at Southern Star Navigation today

Let Bethany review your current shipping program, explain how today’s market affects your specific lanes and volumes, and help put together a strategy that keeps your cargo moving and your costs under control.

Southern Star Navigation is a full-service freight and logistics company providing ocean freight, customs brokerage, and supply chain consulting services. Visit us at southernstarnavigation.com or call Bethany directly at 833-782-7628 Ext. 1 to discuss your shipping needs.