Global Trade and Shipping Updates Impacting Importers and Exporters in 2026

Carriers Push New Rate Actions Across Key Trade Lanes

As we head into mid Q1, ocean carriers are rolling out another round of rate actions on several major trade lanes. The big theme is the same across the board: demand is steady in pockets, but carriers are still working to protect pricing after a long slide in spot markets. For shippers, the practical takeaway is simple: if you move freight on the lanes below, expect more pricing notices and plan for short-term volatility.

Asia → Latin America (including ECSA and other LatAm regions): carriers are again attempting broad general rate increases starting March 1. Even with improving volumes, this lane has seen a steep rate drop over recent months, and a wave of added capacity is creating real headwind for sustained rate lifts. In other words, carriers may announce increases, but the extra vessel space in the market can make it harder for those hikes to “stick.” Indian Subcontinent and Middle East → North America: we’re also seeing peak-season style surcharges and rate adjustments being published for upcoming effective dates. Several notices point to new or revised charges applying from late February into early March, covering shipments moving into U.S. and Canada gateways (depending on carrier scope and coast). If you ship these lanes, it’s a good time to confirm with your carrier or forwarder what’s being applied to your specific origin and destination pairs.

The bottom line is this is a market where carriers are actively testing price increases, but results will depend on how much capacity is actually in the trade and how quickly volumes rebound after Lunar New Year. If you have March sailings in motion now, budgeting for potential add-ons and validating your rate confirmations early can help avoid surprises.

Have upcoming shipments on these lanes? Call us at 833-782-7628 Ext. 1 if you want to walk through current rates or surcharges.

Panama Supreme Court Ruling Shakes Up Canal Container Terminals

Beyond Panama, this ruling highlights a bigger shift in how strategic infrastructure is being viewed. It also affects CK Hutchison’s plans to sell parts of its global port business, which included the Panama terminals. For shippers and logistics providers, the message is that ports are no longer just commercial assets. Legal frameworks, government oversight, and geopolitical concerns are now playing a much larger role in shaping long term port operations and investment decisions.

Panama’s Supreme Court has ruled that the contract allowing Panama Ports Company, a unit of CK Hutchison Holdings, to operate the Balboa and Cristóbal container terminals at both ends of the Panama Canal is unconstitutional. The court said there were legal issues with how the concession was extended and approved. These two terminals are critical gateways for global trade, so the decision immediately caught the attention of the shipping and logistics industry. Panama’s president has stated that port operations will continue without disruption while the government works through next steps.

U.S.–India Trade Deal: What We Know So Far

On February 2nd, President Trump shared a post on Truth Social stating that the United States and India have reached a new trade agreement following a call with Indian Prime Minister Narendra Modi. According to the post, the deal would include lower U.S. reciprocal tariffs on Indian goods, a rollback of an additional tariff layer, and commitments by India to reduce both tariffs and non-tariff barriers on U.S. exports. The announcement also mentioned India increasing purchases of U.S. products such as energy, technology, and agriculture. That said, it’s important to separate announcements from actual policy changes. As of today, no official Executive Order, White House Fact Sheet, USTR release, Federal Register notice, or CBP guidance has been published to implement these updates. This means nothing has changed yet from a compliance or customs standpoint. For now, this should be viewed as a policy signal, not a regulatory change. We’ll continue monitoring official sources and will share updates once anything becomes formal and enforceable.

U.S. and El Salvador Sign New Reciprocal Trade Agreement

Beyond tariffs, the agreement also covers key areas like customs procedures, digital trade, labor standards, environmental protections, and national security cooperation. It includes commitments around fair regulatory practices, rules of origin, and preventing trade circumvention or unfair pricing. For companies doing business in Central America, this agreement doesn’t change operations overnight, but it does set the direction for how U.S.–El Salvador trade will be managed going forward and signals deeper economic alignment between the two countries.

On January 29, 2026, the United States and El Salvador signed a new Agreement on Reciprocal Trade, making this the first such agreement signed in the Western Hemisphere under the current trade framework. The agreement updates how tariffs are applied to certain goods and is designed to reduce trade barriers while strengthening long-standing supply chain links between the two countries. In simple terms, it is a new government-level deal meant to make trade more balanced, more predictable, and more favorable for U.S. exporters and producers.

U.S. and Guatemala Sign New Reciprocal Trade Agreement

On January 30, 2026, the United States and Guatemala officially signed a new Agreement on Reciprocal Trade, marking a formal update to their trade relationship. The agreement sets out revised reciprocal tariff treatment for certain goods and builds on the existing CAFTA-DR framework, while going further in areas like market access, customs procedures, and non-tariff barriers. In simple terms, this is a new government-level deal designed to reduce trade friction, improve fairness, and strengthen supply chain ties between the two countries.

Beyond tariffs, the agreement also includes commitments around labor standards, environmental protections, intellectual property, digital trade, customs facilitation, and even national security cooperation. It gives both countries tools to address transshipment, unfair trade practices, and regulatory barriers, while encouraging more predictable and transparent trade rules. For importers and exporters with activity in Central America, this is worth paying attention to. It doesn’t change anything overnight, but it sets the framework for how U.S.–Guatemala trade will be handled going forward and signals deeper economic alignment in the region.

Read the full announcement from USTR here.

Red Sea Transit Returns (Cautiously)

For shippers, this is an important development, especially for cargo moving on India-to-Europe and Middle East-to-Europe lanes, particularly into the Mediterranean and Southern Europe. A return to the Suez route can significantly reduce transit times compared to the longer Cape of Good Hope diversion used over the past year. That said, carriers are making it clear this is a cautious and limited restart, and future routing will remain dependent on security conditions in the region.

Maersk and Hapag-Lloyd announced this week that one of their shared Gemini services will begin transiting the Red Sea and Suez Canal again, starting mid-February. The service in scope is the IMX route, which connects India and the Middle East with the Mediterranean. According to both carriers, all passages will be supported by naval security, and additional services may follow later if conditions remain stable.

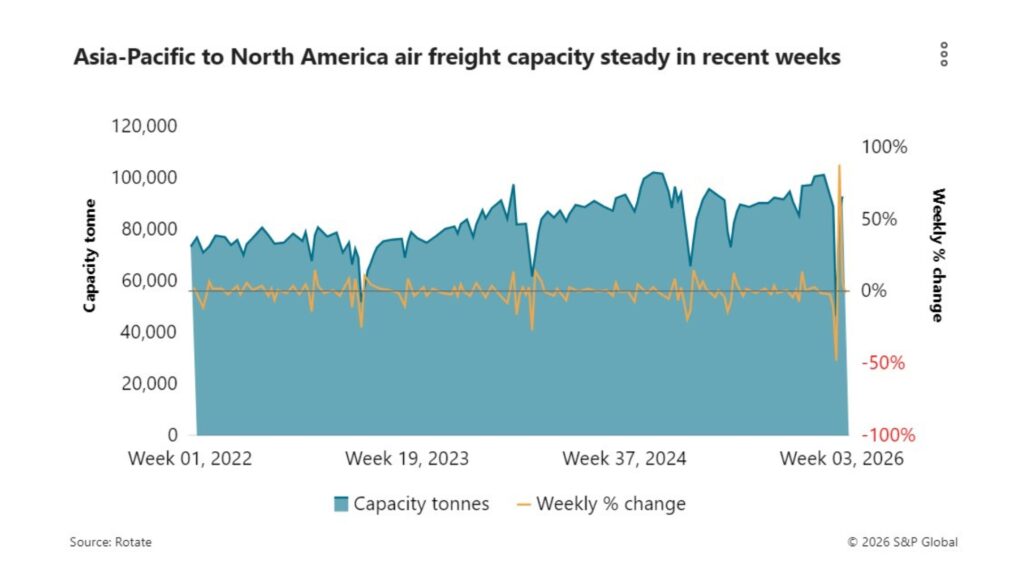

Air Freight Demand Holds Steady Ahead of Lunar New Year

Air freight demand out of Asia has remained steady so far this year, and early signs point to a more muted Lunar New Year peak compared to past years. With the holiday starting on February 17, volumes are expected to rise gradually over the next two weeks rather than spike sharply. Demand has been solid in January on key lanes from China to Europe and from Southeast Asia and Taiwan to the United States, but overall activity is being described as stable rather than exceptional.

While total Asia to U.S. air capacity is lower than last year, some shifts are clearly happening within the region. Vietnam and Taiwan continue to see strong outbound demand, especially tied to technology and electronics shipments, while Chinese exports to the U.S. have softened following recent tariff and de minimis changes. Rates on major Asian export lanes have been holding at healthy levels and are slowly edging up as capacity tightens on certain routes. The overall outlook for 2026 points to moderate growth, with demand expected to stay steady and increasingly shaped by trade policy, geopolitics, and shifting supply chains rather than seasonal surges alone.

CBP’s 2026 Tariff Overview: What Changed, What Didn’t, and Why It Matters

U.S. Customs and Border Protection released an updated Tariff Overview on January 29, 2026. At a high level, nothing new was imposed. There are no new tariff rates, no new deadlines, and no new regulatory requirements tied to this update. This document is meant to be a consolidated, high-level reference that pulls together guidance that already exists across different CBP programs.

What is new is how everything is organized and presented. The biggest addition is that Section 232 Semiconductors are now formally included in CBP’s core tariff guidance. This is important because it moves semiconductors from being an “emerging topic” discussed in scattered memos and FAQs into a standard compliance category that CBP clearly recognizes as part of its main tariff framework.

The updated overview also reaffirms prior CBP FAQ guidance from 2025 around unstacking rules and how certain IEEPA programs (including Brazil, Russian Oil, and CA/MX measures) may apply in specific “content vs product” scenarios. In simple terms, this supports CBP’s position that some tariffs can apply to non-steel, non-aluminum, or non-copper content within a finished product, depending on how the item is structured and classified.

So while this update does not change policy, it does matter from a practical standpoint. This is the kind of document that auditors, brokers, and compliance teams will likely use as a baseline reference going forward. For importers, it’s a good reminder to review product classifications, material content, and how duty stacking is being modeled in landed cost calculations. It’s not an urgent alert, but it is a strong resource and a useful snapshot of how CBP is currently framing today’s tariff landscape.

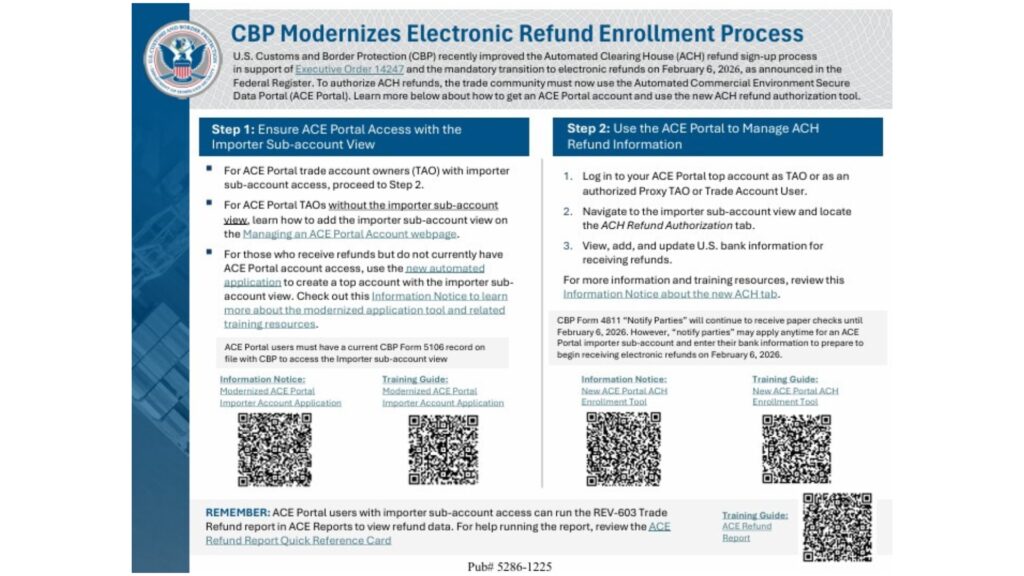

CBP Electronic Refunds Now Live as of February 6

For importers and trade partners, this is an operational change that requires action. To receive refunds without delays, companies must be properly enrolled for ACH refunds through the ACE Portal and make sure their account and banking information is accurate and up to date. CBP has released new FAQs, reference guides, and training resources to help with the transition. This doesn’t change refund eligibility, but it does change how the money is delivered, so confirming your setup now is important to avoid missed or delayed refunds.

As of February 6, 2026, U.S. Customs and Border Protection is now issuing all refunds electronically through ACH (Automated Clearing House), with only very limited exceptions. This change comes from CBP’s Electronic Refunds Interim Final Rule and means paper refund checks are no longer the standard method. Going forward, refunds for duties, fees, and other CBP payments will be sent directly to the bank account on file.

CBP Trade Statistics: What the Latest Numbers Tell Us About Enforcement

CBP recently released updated trade statistics that show just how large and complex U.S. trade has become. In fiscal year 2025, CBP processed over $3.6 trillion in imports, handled more than 50 million entry summaries, and collected about $216 billion in duties, taxes, and fees. These numbers highlight the massive volume moving through U.S. ports and the role CBP plays in keeping trade flowing while also protecting U.S. businesses and consumers.

The enforcement side of the data is just as important. Billions of dollars continue to be collected under trade remedy programs like Section 232, Section 301, and IEEPA, with major activity tied to steel, aluminum, autos, copper, China-origin goods, and new reciprocal tariffs. CBP also completed hundreds of audits, recovered billions through post-entry reviews, issued thousands of penalties, and seized billions of dollars in counterfeit and unsafe products. The takeaway is simple: enforcement today is increasingly data-driven and post-release. For importers, the risk is no longer just at the port, it often shows up months later through audits, reviews, and penalties.

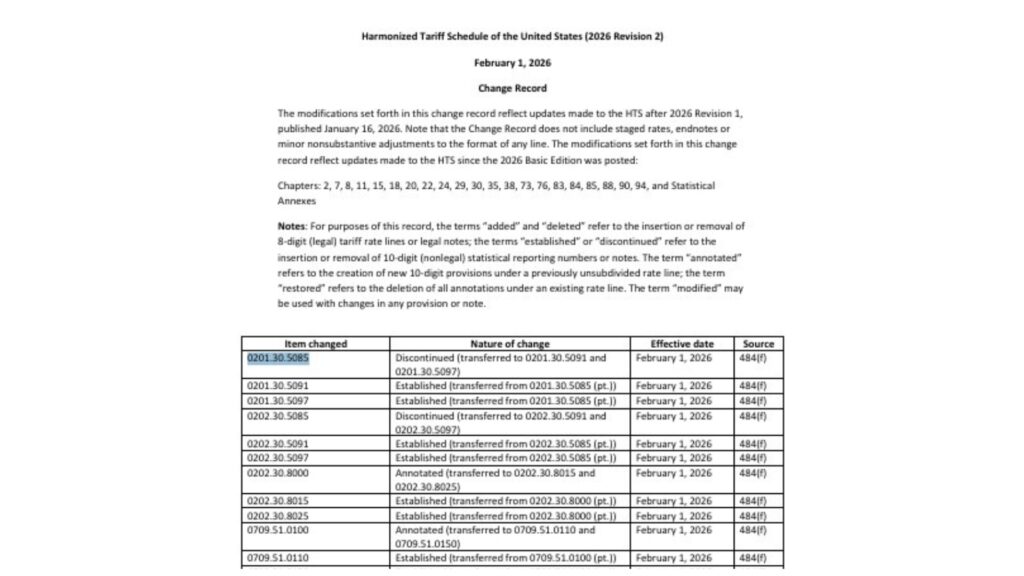

HTS Classification Update Now in Effect (February 1, 2026)

U.S. Customs implemented the 2026 HTS Revision 2 updates on February 1, introducing dozens of classification changes across a wide range of product categories, including food products, chemicals, machinery, electronics, metals, and industrial components. These updates include discontinued codes, newly established tariff lines, and statistical refinements at the 10-digit level. While most of the changes do not directly impact duty rates, they do affect how products must now be declared on entries.

For importers, the real risk is operational. Continuing to use outdated HTS codes can lead to entry rejections, post-entry corrections, compliance flags, or inaccurate duty reporting. If your products fall within affected chapters, it’s a good time to validate current classifications and ensure internal systems, broker templates, and product databases reflect the latest HTS structure now in force.